How much do credit inquires effect credit score for mortgage approval?

Short Answer:

It depends upon the number and when they are pulled. For hard credit inquires, like inquires in a short period of time will be considered one inquiry against your credit score. What is a short period of time? Undefined. But I believe its within 21 days. Therefore, if you have a hard credit pulled on May 1st and then another on June 2nd that would be considered 2 inquires. The more inquires you have in a 24 month period will decrease your score. Credit inquires account for ~10% of your credit score.

Longer Answer:

Recently, I was teaching a class to Realtors on the pre-approval process. As we discussed the credit piece of the pre-approval process, one attendee asked, "what is the period of time that our clients can have their credit pulled and have only one inquire?" The answer isn't so easy. Let me explain:

What Are Credit Inquiries?

Credit inquiries occur when a lender or financial institution checks your credit report as part of their credit decision-making process. There are two types of credit inquiries:

- Hard Inquiries: These occur when a lender checks your credit report to make a lending decision, such as when you apply for a mortgage, car loan, or credit card. Hard inquiries leave a mark (an inquiry) on your credit report for 24 months. The inquiry can affect your credit score.

- Soft Inquiries: These occur when you or a company checks your credit report for non-lending purposes, such as background checks, pre-approved credit offer, approval for ulitilies or cell phone plans. Soft inquiries do not affect your credit score.

How Do Hard Inquiries Affect Your Credit Score?

Hard inquiries can have a small, temporary impact on your credit score. Here’s how:

- Score Impact: A single hard inquiry can lower your credit score by a few points, typically between 3 to 10 points. However, the impact can vary based on your overall credit profile.

- Duration: The effect of a hard inquiry usually lasts for about 12 months, although it can stay on your credit report for up to two years. As time goes on from the date of the inquiry, the effect reduces.

- Multiple Inquiries: If you’re shopping around for a mortgage or a car loan and multiple lenders check your credit within a short period (usually 14 to 21 days), these inquiries are often treated as a single inquiry to minimize the impact on your credit score. This is known as rate shopping.

Why Do Hard Inquiries Affect Your Credit Score?

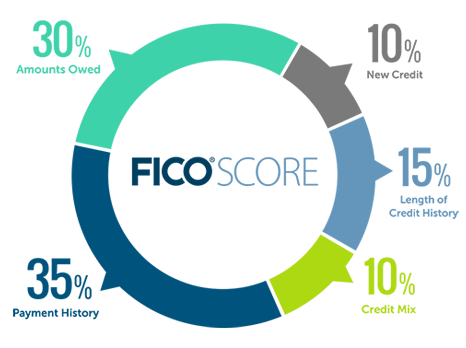

Credit scoring models, like FICO and VantageScore, consider hard inquiries as potential indicators of risk. When you apply for new credit, it suggests that you might be taking on additional debt, which could affect your ability to repay existing obligations. Too many inquires outside of the "short period of time" may be an indication that you aren't being approved for credit.

The impact is generally minor compared to other factors like payment history, credit utilization, and length of credit history. Most models on credit count credit inquires for around 10% of the score. (We are 100% sure, as the three credit burueas keep their alogrithom to themseleves.)

Tips to Minimize the Impact of Credit Inquiries

- Limit Applications: Only apply for credit when necessary. Each hard inquiry can slightly lower your score, so avoid unnecessary applications.

- Rate Shopping: If you’re shopping for a mortgage, try to do it within a short time frame. Credit scoring models will recognize that you’re rate shopping and will count multiple inquiries as a single one.

- Check Your Credit Report: Regularly review your credit report to ensure there are no unauthorized inquiries. You can get a free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once a year at AnnualCreditReport.com.

- Maintain Good Credit Habits: Focus on the bigger picture by maintaining good credit habits, such as paying bills on time, keeping credit card balances low, and managing debt responsibly.

Conclusion

While hard inquiries can affect your credit score, the impact is generally minor and short-lived. Having a creditor run a hard credit report should have minimum impact to your credit score. However, Be careful on who, when and how many people run your credit score.

Have additional questions about credit inquires, I am happy to answer them. Reach out to me at teamjd@mainstreethl.com

—

This blog is for informational purposes only. Make sure you understand the features associated with the loan program you choose, and that it meets your unique financial needs. Subject to Debt-to-Income and Underwriting requirements. This is not a credit decision or a commitment to lend. Eligibility is subject to completion of an application and verification of home ownership, occupancy, title, income, employment, credit, home value, collateral, and underwriting requirements. Not all programs are available in all areas. Offers may vary and are subject to change at any time without notice. Should you have any questions about the information provided, please contact me.